Value at Risk (VaR)

Understand your downside before it becomes your problem.

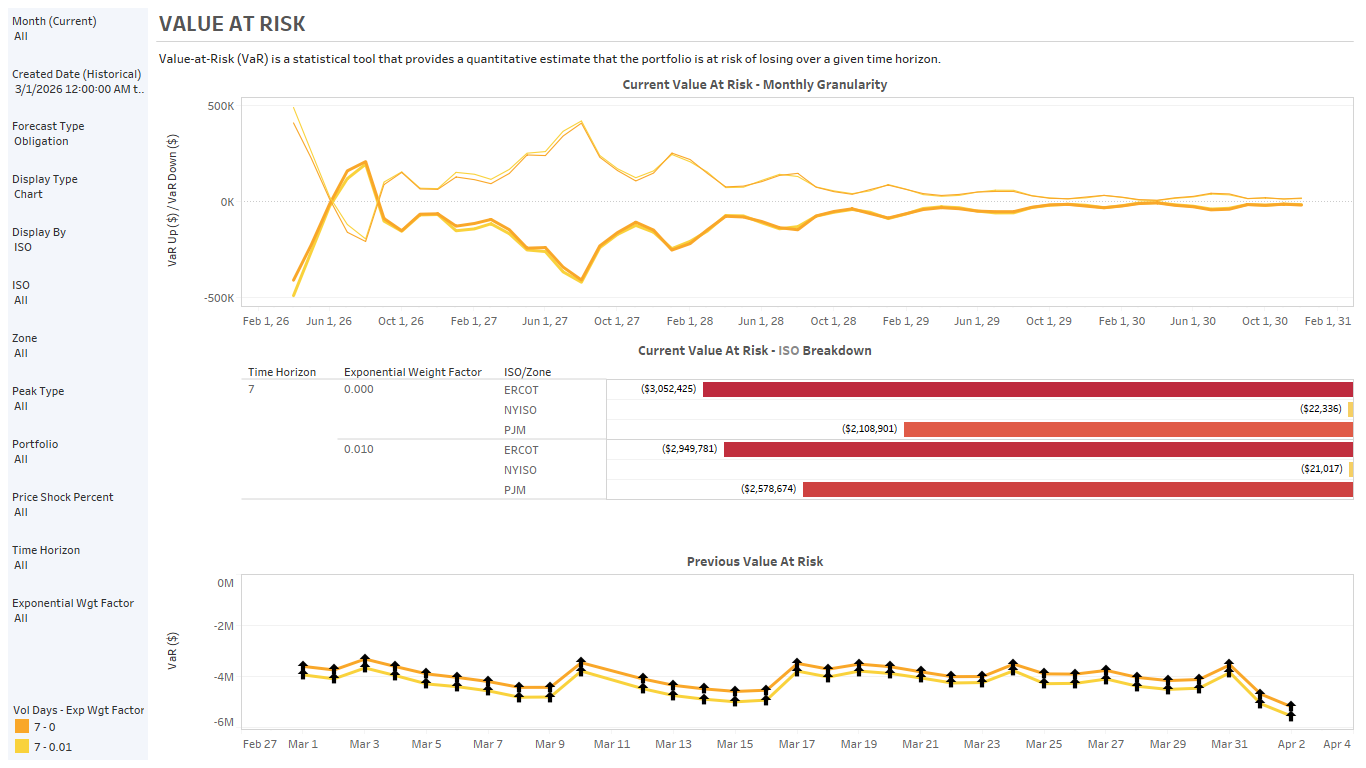

Multi-Scenario Risk Modeling at Your Fingertips

Quantify portfolio losses under various market scenarios — and choose the methodology that fits your risk appetite.

Risk360's VaR module quantifies potential portfolio losses under various market scenarios. Whether you prefer historical simulation, Monte Carlo, or parametric approaches, the platform supports multiple methodologies and lets you compare results side by side. Choose the methodology that matches your risk philosophy — then trust the numbers.

Configurable confidence intervals, holding periods, and stress scenarios give you the flexibility to model risk the way your organization thinks about it. The output feeds directly into position management and executive reporting — so risk limits aren't just set, they're monitored in real time.

Key Capabilities

- Historical simulation, Monte Carlo, and parametric VaR methodologies

- Configurable confidence intervals and holding periods

- Stress testing with custom and historical scenarios

- Portfolio-level and component-level risk decomposition

- Real-time monitoring against risk limits and triggers

- Executive-ready reporting with drill-down capability

MANAGE YOUR RISK

Related Risk360 Capabilities

Explore the other modules in Risk360's risk management suite.

See Value at Risk in Risk360.

30 minutes. Your data. No vendor speak.

Talk to Our Team →